Hyperliquid is facing a growing set of regulatory constraints in the US and UK, even as the decentralized perpetuals venue continues to attract major market attention. Derek Edwards, managing partner at Collab+Currency and co-founder of Glitch Marfa, said the project now appears to have five possible routes as US oversight of crypto perps begins to harden.

In a post on X, Edwards described Hyperliquid as “a killer product,” but argued that its path into the US market is being complicated across three layers: the product layer, the network and token layer, and the collateral layer. The immediate backdrop is a shifting US derivatives regime after the CFTC approved Kalshi’s BTCPERP contract and separately cleared a path for certain Coinbase-linked Deribit perpetuals to be treated as foreign futures.

That matters because Hyperliquid’s core product sits directly in the part of the market regulators are now bringing onshore. As Edwards framed it, regulated distribution of perps in the US may require “a fully regulated venue, compliant customer funds path, approved product scope, surveillance, disclosures, and accountable corporate counterparties.” Without that infrastructure, he warned, offering Hyperliquid liquidity to US customers could be viewed as routing users into an unapproved offshore venue.

The 5 Options For Hyperliquid

The first option, in his view, is the simplest but most limiting: Hyperliquid could ignore the US market and remain offshore. Edwards compared that route to Binance’s main exchange, which eventually had to more aggressively block American users after years of lighter restrictions. Such an approach could preserve Hyperliquid’s current product experience, but it would also leave US institutional access on the table.

The second route would be a US regulated wrapper. Under that model, the main offshore venue would continue serving global crypto-native users, while a separate affiliate or partner offered regulated perps through a compliant structure. Edwards called this “Hyperliquid US ” and said that “in a perfect world” it would be the ideal outcome for targeting US users. But the tradeoff would likely be a meaningful separation of customer funds, product scope and HYPE value capture from the main network.

” and said that “in a perfect world” it would be the ideal outcome for targeting US users. But the tradeoff would likely be a meaningful separation of customer funds, product scope and HYPE value capture from the main network.

That separation is central to the securities-law concern. If revenue from a regulated corporate venue flowed into buybacks, burns or assistance-fund mechanics, Edwards argued, it could begin to look as though token holders were economically participating in the profits of an operating company. “Net net,” he wrote, “this model would likely require a significant rewrite of how the Hyperliquid network works for US participation.”

A third path would be decentralization under the CLARITY Act framework. Edwards said the bill offers a major potential route for protocols to “progressively decentralize” until a network and token are no longer under “coordinated control.” In theory, that could help a token shift from a securities framework toward a digital commodity classification.

For Hyperliquid, however, Edwards argued that this route would carry operational costs. The project would likely need to broaden validators, decentralize listings, decentralize oracle and risk controls, reduce emergency discretion, dilute controlled ownership and make upgrades more governance-driven. That would be a significant change for a platform whose market appeal has partly rested on fast product decisions by a highly capable core team.

Crucially, he added, decentralization would not solve everything. “The clarity act’s decentralization framework is not a DCM/DCO workaround. Even if the hyperliquid network could eventually satisfy clarity’s decentralized governance framework, this would still not automatically permit hyperliquid to offer perps directly to US users.” In other words, token classification and derivatives-market access remain separate problems.

The fourth route would be the most compliant but also the most damaging to the current network thesis: centralize the company, restructure HYPE as a security and move value capture toward equity, licensing or regulated-entity revenue. Edwards called this “probably the weakest option game theoretically,” because it would cut against the idea that protocol activity and economics are aligned around HYPE as a digital commodity. The fifth option is lobbying. Edwards pointed to policy work around Hyperliquid as evidence that the industry may push for a bespoke framework for crypto-native perp venues. Still, he cautioned that even a more flexible CFTC approach would not automatically resolve HYPE’s classification under CLARITY.

The pressure is not purely theoretical. CME Group and Intercontinental Exchange have already urged US regulators to scrutinize Hyperliquid over market-manipulation and sanctions-evasion risks, while the UK Financial Conduct Authority warned in May that Hyperliquid may be providing or promoting financial services without authorization. Meanwhile, Coinbase’s move to become the official treasury deployer of USDC on Hyperliquid deepens the protocol’s connection to US-regulated infrastructure at the collateral layer.

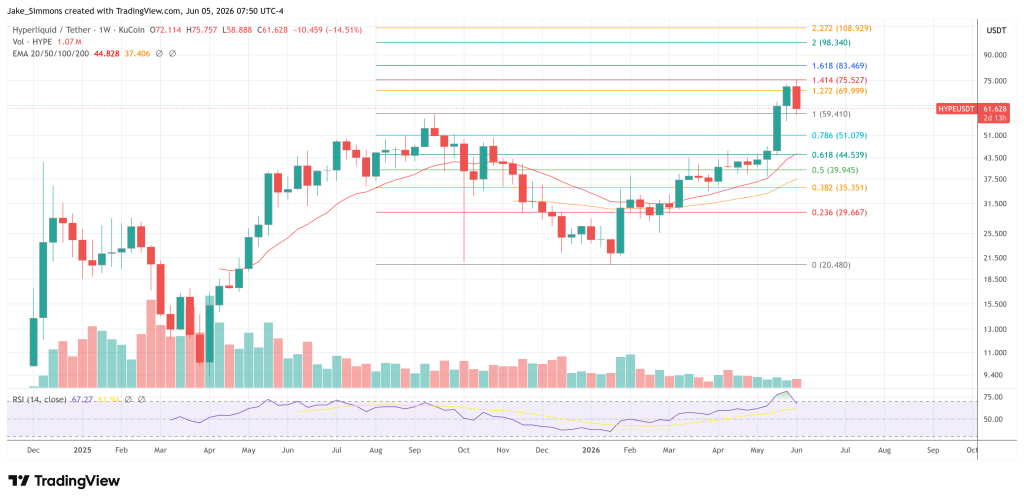

At press time, HYPE traded at $61.628.

You can get bonuses upto $100 FREE BONUS when you:

💰 Install these recommended apps:

💲 SocialGood - 100% Crypto Back on Everyday Shopping

💲 xPortal - The DeFi For The Next Billion

💲 CryptoTab Browser - Lightweight, fast, and ready to mine!

💰 Register on these recommended exchanges:

🟡 Binance🟡 Bitfinex🟡 Bitmart🟡 Bittrex🟡 Bitget

🟡 CoinEx🟡 Crypto.com🟡 Gate.io🟡 Huobi🟡 Kucoin.

Comments